Did you know that 70% of businesses shipping valuable goods have inadequate freight insurance coverage? Surprisingly, many shippers discover this painful truth only after experiencing a significant loss.

Navigating the complex world of cargo insurance often feels overwhelming. From understanding freight liability limits to managing insurance claims effectively, the entire process requires careful planning and risk management. Unfortunately, carrier liability alone typically covers just a fraction of your shipment’s actual value.

This step-by-step guide will walk you through everything you need to know about selecting the right freight insurance for your specific needs. We’ll explore different coverage types, help you assess your unique requirements, and provide practical tips for choosing trustworthy insurance providers. Let’s ensure your shipments stay protected during their journey!

Understanding Freight Insurance Basics

Freight insurance serves as a safety net for businesses shipping goods across global supply chains. Unlike many assume, it’s not automatically included in standard shipping arrangements, but rather requires deliberate consideration and purchasing decisions.

What freight insurance actually covers

Freight insurance (also called cargo insurance or goods-in-transit insurance) protects the financial value of shipments against a wide spectrum of risks encountered during transit. This policy safeguards your cargo from origin to destination regardless of transportation mode—whether by sea, air, road, or rail.

A comprehensive freight insurance policy typically covers:

- Physical damage from accidents, rough handling, or extreme weather events

- Theft, pilferage, and non-delivery of goods

- Natural disasters including fires, floods, and severe weather

- Loading and unloading errors

- Infestation and abandonment

- Customs rejection and certain delays

- Fraud and other specified issues

Nevertheless, standard policies often exclude certain scenarios. These frequently include wear and tear, improper packaging, employee dishonesty, delay-related losses, war, strikes, or civil unrest—unless specifically added to your policy. Always review your policy documents thoroughly to understand specific exclusions.

The cost of freight insurance generally ranges between 0.3% to 0.5% of the commercial invoice value of the goods [1], making it a relatively small investment compared to potential losses.

How it differs from carrier liability

Many shippers mistakenly believe carrier liability offers sufficient protection, yet the differences are substantial and critically important to understand.

Carrier liability represents the minimum coverage provided by transportation companies as required by law. This protection comes automatically with your shipment and is typically built into your rate. However, carrier liability:

- Often undervalues your freight, sometimes covering as little as $0.25 per pound for LTL shipments [2]

- Places the burden of proof on you to demonstrate carrier negligence

- Requires filing claims within strict timeframes (typically nine months) [3]

- Excludes numerous scenarios including acts of God, improper packaging, and concealed damage

- Necessitates filing separate claims with each carrier involved in handling your cargo

Conversely, freight insurance offers significantly broader protection. With freight insurance, you need only prove damage or loss occurred—not who was at fault. Claims are typically processed within 30 days [3] rather than the 120 days carriers may take, and coverage extends to scenarios excluded under carrier liability.

Why it matters for shippers

Freight insurance matters fundamentally because it transfers financial risk from your business to an insurance company, protecting your bottom line when unexpected events occur.

Consider that carrier liability frequently covers just a fraction of your goods’ actual value. For heavy yet valuable items like textbooks, the standard $0.25 per pound compensation [3] would be woefully inadequate to cover replacement costs.

Furthermore, the shipping environment contains numerous risks beyond anyone’s control—from natural disasters to geopolitical events. Without adequate insurance, businesses face potentially devastating financial consequences when shipments are lost, damaged, or stolen.

Freight insurance additionally enhances business stability by:

- Ensuring predictable financial outcomes regardless of shipping mishaps

- Fulfilling contractual obligations that often require comprehensive coverage

- Maintaining positive customer relationships through prompt replacements

- Providing peace of mind throughout complex supply chains

- Enabling expansion into new markets or shipping lanes with confidence

Consequently, freight insurance should be viewed not as an optional expense but as an essential risk management tool—particularly for high-value, fragile, or time-sensitive shipments.

By thoroughly understanding the fundamentals of freight insurance coverage, businesses can make informed decisions that protect their cargo, reputation, and financial stability throughout the shipping journey.

Types of Freight Insurance Policies

Selecting the right freight insurance policy requires understanding the distinct types available in the market. Each policy type offers different levels of protection, exclusions, and premium costs. Let’s examine the six main categories of freight insurance policies to help you make an informed decision.

Basic coverage

Basic freight insurance, often referred to as limited liability coverage, provides the minimum level of protection for your shipments. This standard coverage typically includes loss or damage during transportation, albeit with predetermined limits that may not reflect your cargo’s actual value. Basic coverage is commonly offered by carriers as their default insurance option.

The protection is restricted to specific scenarios, typically covering damage from accidents or natural disasters while excluding issues like careless handling. For many shippers, basic coverage serves as an entry-level option when transporting low-value goods through relatively safe routes.

Named perils coverage

Named perils insurance (also called specified perils) protects your cargo exclusively against hazards explicitly listed in your policy document. If damage occurs from a cause not specifically named, the insurer bears no responsibility for compensation.

For example, a named perils policy might cover damage from tornadoes and hurricanes but exclude flooding or theft. These policies are often designed around specific cargo types, making them suitable for shippers with clearly identified risks. In marine cargo insurance, four perils are usually covered: burning, sinking, collision, and stranding.

Broad coverage

Sitting between basic and all-risk options, broad freight insurance offers more comprehensive protection while maintaining specific exceptions. This policy type compensates for all damage or loss to your cargo except for particular exclusions stated in the policy.

Broad coverage frequently excludes personal items like electronics or currency. For businesses shipping commercial goods without unusual risk factors, broad coverage presents a balanced approach to freight protection—offering substantial security without the premium cost of all-risk policies.

All-risk coverage

Despite its name, all-risk insurance doesn’t cover everything. Instead, it provides the most comprehensive protection available, covering physical loss or damage from any external cause unless specifically excluded in the policy. All-risk policies protect against accidental damage, theft, fire, natural disasters, and other unforeseen events during transit.

Common exclusions include war, intentional damage, normal wear and tear, improper packaging, and governmental interference. For high-value, fragile, or time-sensitive shipments, all-risk coverage offers the greatest peace of mind, albeit at higher premium costs.

Total loss-only coverage

As its name suggests, total loss-only (TLO) insurance activates exclusively when the entire shipment is compromised rather than when individual items are damaged. This policy type is designed to protect against catastrophic events resulting in complete destruction or loss of cargo.

TLO coverage typically includes protection against derailment, collision, fire, lightning, hurricanes, floods, earthquakes, and sinking vessels. As a more affordable alternative to all-risk insurance, TLO coverage works well for bulk shipments, used merchandise, or when you’re handling loading/unloading yourself.

Contingent coverage

Contingent cargo insurance functions as a supplementary safety net, filling gaps in your primary insurance policy. This coverage activates when your primary insurer denies a claim or when losses exceed your policy limits.

Primarily designed for transportation intermediaries like freight brokers and 3PLs, contingent coverage protects against carrier liability failures. For instance, if a carrier’s insurance lapses or excludes specific damage types (like refrigeration equipment failure), your contingent policy would cover the loss. This additional layer of protection proves particularly valuable when working with multiple carriers or handling high-value shipments.

Understanding these policy types enables you to select coverage that aligns with your specific shipping needs, cargo value, and risk tolerance.

What Freight Insurance Does and Doesn’t Cover

Understanding the fine print of your freight insurance policy is essential for avoiding unpleasant surprises when filing claims. Let’s examine exactly what these policies typically cover—and what they don’t.

Common inclusions like theft and damage

Most freight insurance policies provide protection against:

- Physical damage from collisions, drops, and rough handling

- Theft, pilferage, and mysterious disappearance of goods

- Natural disasters including storms, floods, and earthquakes

- Damage during loading and unloading operations

- Water damage from heavy rain or vessel leaks

- Fire and smoke damage

- Temperature damage (with appropriate endorsements)

Standard cargo insurance typically covers the commercial invoice value of the goods plus freight charges and insurance costs—essentially making you “whole” after a loss. Moreover, comprehensive policies often include protection during storage at intermediate points, though typically limited to 30-60 days.

Typical exclusions to watch for

Even all-risk policies have limitations. Freight insurance policies routinely exclude:

- Inadequate packaging – Damages resulting from poor packing materials or methods

- Inherent vice – Deterioration due to the natural characteristics of the product

- Ordinary leakage – Normal product loss during transit

- Delay – Financial losses caused by late deliveries (unless specifically endorsed)

- War and strikes – Though available as separate endorsements

- Employee dishonesty – Theft by your own staff

- Pre-existing damage – Issues present before transit began

- Rejected shipments – Unless covered by specific return shipment clauses

Importantly, most insurers require proof that damage occurred during transit rather than before shipping or after delivery. This makes thorough documentation of your shipment’s condition at all stages crucial for successful claims.

Goods often excluded from coverage

Certain cargo types often require specialized coverage beyond standard policies:

First, high-value items like jewelry, precious metals, and fine art typically need declared-value coverage with additional premiums. Second, hazardous materials face stringent insurance requirements and higher rates due to increased risk.

Additionally, perishable goods usually require specific temperature control endorsements, while used or refurbished merchandise often receives substantially limited coverage—sometimes as little as 50% of invoice value.

Other challenging categories include:

- Live animals (requiring specialized transit insurance)

- Personal effects (excluded from most commercial policies)

- Currency and negotiable instruments

- Mobile phones and electronics (often subject to higher premiums)

- Antiques and collectibles (requiring professional appraisals)

The exclusion of these items stems primarily from their heightened risk profiles or valuation challenges. For such shipments, working with specialized insurance providers or seeking specific endorsements becomes necessary.

Before finalizing your freight insurance, thoroughly review all exclusions and limitations. Ask potential insurers about their specific handling of your cargo type and request written confirmation of coverage for any concerns. This proactive approach helps ensure your shipments have appropriate protection throughout their journey.

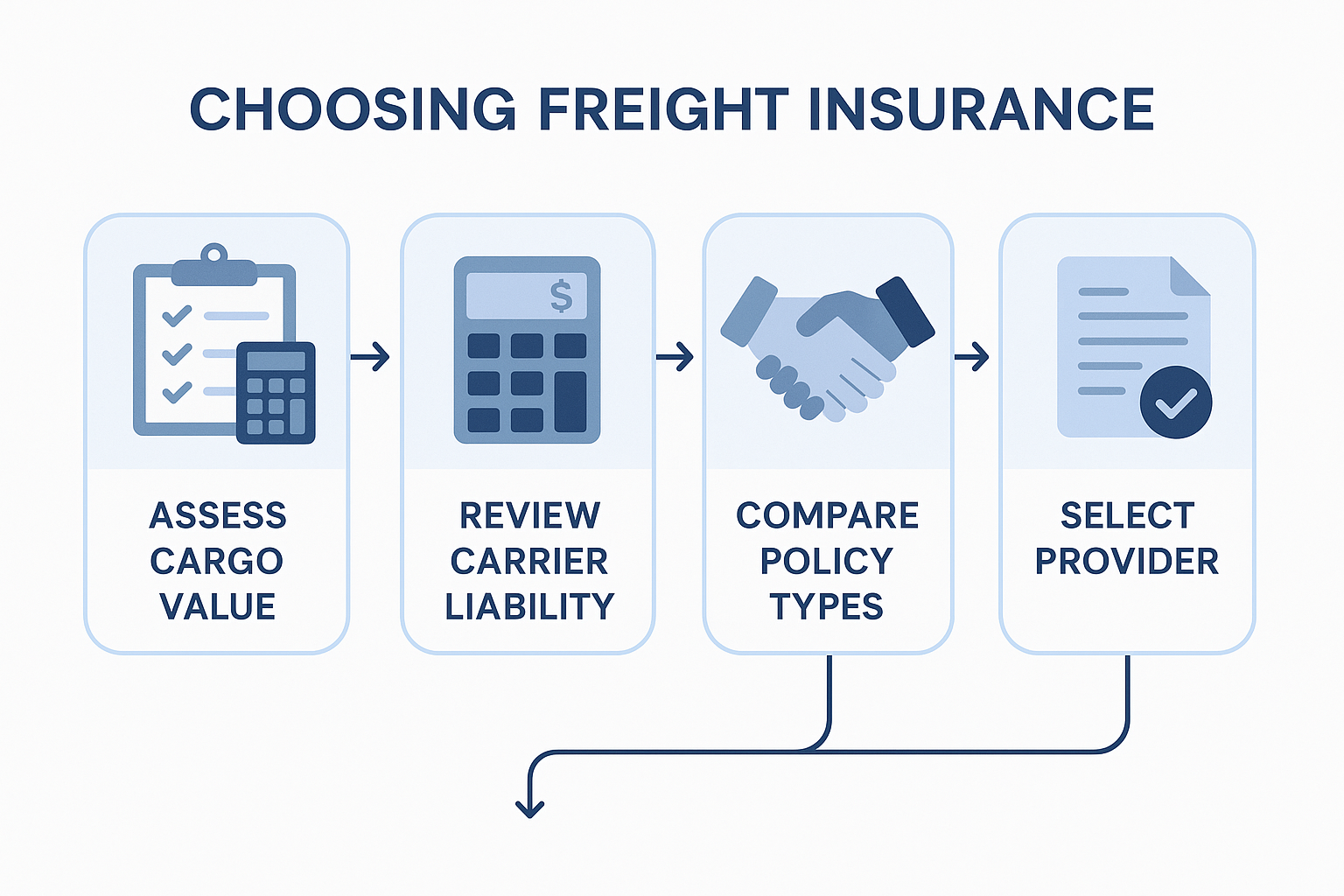

How to Evaluate Your Insurance Needs

Properly evaluating your freight insurance needs requires a systematic approach to risk assessment. Following a strategic process helps determine the optimal coverage for your specific shipping circumstances.

Assessing the value and risk of your goods

Begin by accurately calculating the true value of your shipments. Underestimating cargo value leads to insufficient coverage, whereas overestimating results in unnecessarily high premiums [4]. Most policies should, at minimum, cover the commercial invoice value plus freight charges [5].

Consider these key factors when evaluating cargo risk:

- Inherent characteristics: High-value, perishable, or fragile items require more comprehensive coverage than durable, low-value goods [6]

- Susceptibility to damage: Items prone to breaking, spoiling, or theft (known as “inherent vice”) need specialized protection [6]

- Replacement costs: Insurance should reflect what it would cost to replace items—not just their wholesale value [7]

Understanding your shipping routes and modes

Each transportation method presents unique risks requiring specific insurance considerations:

- Road transit: Policies must address traffic accidents, theft risks, and varying road conditions

- Rail transit: Coverage should focus on derailment risks and terminal handling damage

- Sea transit: Marine cargo insurance must account for sinking, piracy, and saltwater damage

- Air transit: Air shipments face risks from pressure changes, rough handling, and accidents [8]

Additionally, certain shipping routes carry elevated risks. Areas with political instability, severe weather patterns, or high theft rates typically increase premium costs [4]. Accordingly, shippers should evaluate route-specific hazards when determining coverage needs.

Checking your carrier’s liability limits

Analyzing carrier liability limitations is perhaps most crucial, since these represent the maximum amount a carrier will pay for damaged freight if found responsible [9]. For LTL shipments, liability varies by carrier, packaging quality, and freight class [7].

Typically, carrier liability covers far less than a shipment’s actual value. Without freight insurance, businesses often find themselves “out of luck in recovering the full value” when damages exceed these limits [7]. Furthermore, carriers can deny liability for numerous exceptions including acts of God, improper packaging, and concealed damage [10].

Full truckload shippers should explicitly inquire about maximum carrier liability and consider purchasing additional coverage when appropriate [7]. Ultimately, comprehensive freight insurance fills these coverage gaps, providing financial protection against scenarios where carrier liability proves insufficient.

Tips for Choosing the Right Policy and Provider

Selecting the right freight insurance partner can make all the difference when disaster strikes your shipments. After determining your coverage needs, focus on finding a provider who delivers both comprehensive protection and excellent service.

Compare multiple insurers and brokers

Finding the ideal freight insurance provider requires thorough research. Start by obtaining quotes from several companies to ensure competitive pricing. Beyond cost considerations, evaluate each insurer’s:

- Financial stability and industry reputation

- Experience with your specific cargo types

- Customer reviews and satisfaction ratings

- Industry certifications and partnerships

“It is important to compare quotes from multiple insurers to ensure that you are getting the best value for your money” [5]. Additionally, examine any supplementary fees or handling charges that might increase your total costs.

Review claim processes and timelines

Examine how potential insurers handle claims, as this ultimately determines how quickly you’ll recover losses. Most quality providers offer expedited payouts “typically in only a few days” [11] versus the 120 days carriers might take. Prioritize companies with:

- Online claims portals for easy documentation submission

- Clear documentation requirements

- Established timelines for claim resolution

- No requirement to prove carrier negligence

Notably, some providers streamline this process through integrations with major carriers and e-commerce platforms, “making the process smoother and more efficient” [12].

Look for transparent terms and exclusions

Carefully review policy terms beforehand to avoid surprises when filing claims. “Make sure you understand what types of losses that the policy does not cover” [5]. Quality providers offer transparent information about coverage limitations without burying crucial details in fine print.

Consider working with a 3PL for added support

Third-party logistics providers can significantly simplify your insurance experience. Many 3PLs offer “managed logistics services [that] take that burden off your plate” [13], handling freight claims and disputes directly with carriers. This arrangement allows you to “stay focused on serving your customers and growing your business” [13] rather than managing complex claims.

Ultimately, the right freight insurance provider combines fair pricing, excellent service, transparent terms, and efficient claims handling—creating a safety net that truly protects your business when shipments go awry.

Conclusion

Choosing the right freight insurance stands as a critical business decision that directly impacts your bottom line and supply chain resilience. Throughout this guide, we’ve examined various aspects of freight insurance, from basic coverage to specialized policies tailored for specific cargo types. Undoubtedly, carrier liability alone leaves most businesses dangerously exposed, covering merely a fraction of actual shipment value.

After analyzing your specific needs carefully, you should therefore assess multiple insurance providers based on their financial stability, claim processes, and policy transparency. Many businesses mistakenly rely on minimal coverage until experiencing a significant loss – a painful lesson that adequate protection costs far less than replacing uninsured cargo.

Remember that freight insurance essentially transforms shipping uncertainties into manageable, predictable expenses. Though policies generally cost between 0.3% to 0.5% of invoice value, this small investment protects against potentially devastating financial losses due to theft, damage, or natural disasters. Additionally, comprehensive coverage ensures business continuity even when shipments encounter unexpected problems.

Finally, consider reviewing your freight insurance strategy annually as your shipping patterns evolve. Routes change, cargo values fluctuate, and new risks emerge – accordingly, your insurance protection should adapt to maintain appropriate coverage. The right freight insurance doesn’t just protect individual shipments but safeguards your business reputation, customer relationships, and long-term profitability in an increasingly complex global supply chain.